Hey! If you’re looking for a zero-commission investment platform that’s easy to use to start your wealth-building journey, you’ve come to the right place! I’m an investor living in Canada, and I’ve been using Wealthsimple since 2020. Starting with just $50 to test the waters, my account has now grown to over $18,000. This article isn’t just a feature overview—it’s my real experience and “lessons learned” accumulated over 5 years.

Bottom line: Wealthsimple is Canada’s most popular zero-commission investment platform, with over 3 million users and $10 billion CAD in assets under management. If you’re living in Canada and want to start investing but don’t know where to begin, this article will be your complete guide.

🎁 Exclusive Sign-Up Bonus

Use my referral code to get a $25 cash bonus:

Hey! Join me on Wealthsimple and get $25 when you fund any account with my referral code HP6BUW 🎁 T&Cs apply

Sign up now: wealthsimple.com/invite/HP6BUW

Table of Contents

🌟 Why Choose Wealthsimple?

💡 A Revolutionary Breakthrough in Canadian Investing

Before Wealthsimple came along, Canadian investors could only trade stocks through traditional banks (like RBC, TD, Scotiabank), which charged a hefty $9.95 commission per trade. I still remember when I first opened an account at a bank—just thinking about paying $10 for each transaction made me hesitant to execute any trades.

Imagine you can only set aside $100 per month for regular investing. A single $10 commission means you’re already losing 10% of your capital right at the starting line! This cost structure mathematically kills the viability of small-amount regular investing.

Wealthsimple changed everything:

- ✅ Completely zero commission on Canadian stocks and ETFs ($0 Commission)

- ✅ Minimum investment of just $1

- ✅ Fractional share trading—buy Tesla with just $10

- ✅ Account setup in under 3 minutes, instant activation

- ✅ All-in-one financial platform: investing, banking, taxes, crypto all in one app

🚀 Major Breakthroughs in 2025

Wealthsimple officially surpassed $100 billion CAD in assets under management in October 2025, achieving their goal a full three years ahead of schedule! It’s also worth noting that Drake became an investor in 2021, when Wealthsimple was already 7 years old with over 2 million users, helping establish Wealthsimple’s unique brand image among younger demographics.

Latest 2025 Features:

- Options Trading Now Fully Available: Options trading features are being rolled out, expected to be fully available between Q4 2025 and Q1 2026, offering $0 commission + $0 contract fees

- Extended Trading Hours: Pre-market and after-hours trading now available

- Gold Trading: Purchase physical gold (1% transaction fee), with the option to have gold coins shipped to you when you reach the threshold (2.25% conversion fee per ounce for coins) in non-registered accounts

- RESP Accounts (Registered Education Savings Plan) officially launched

- Norbert’s Gambit (coming Q1 2026)

💼 Complete Wealthsimple Features Overview

📈 Wealthsimple Trade: Zero-Commission Stock Trading Platform

This is Wealthsimple’s most popular service, allowing you to trade Canadian and US stocks commission-free.

| Feature | Details |

|---|---|

| Trading Options | 14,000+ Canadian and US stocks/ETFs |

| Trading Fees | CAD stocks $0, USD stocks $0 (but 1.5% FX fee applies) |

| Fractional Shares | Buy fractional shares of high-priced stocks with as little as $1 |

| Auto-Investing | Set up automatic purchases weekly/bi-weekly/monthly |

| Dividend Reinvestment | DRIP feature automatically reinvests dividends, supports fractional shares |

| Options Trading | Fully launched in October 2025, $0 commission per contract |

| Gold Trading | Purchase physical gold stored in Canada, minimum $1 (1% trading fee); redeem as Royal Canadian Mint coins when threshold is reached (non-registered accounts only) |

🎯 Fractional Share Trading: Big Opportunities for Small Capital

This is what I consider the most revolutionary feature! In the past, if you wanted to invest in Tesla but the stock price was too high, you had to buy whole shares. If one Tesla share cost $400 and you only had $150 in your account, you simply couldn’t invest.

Wealthsimple’s fractional share trading makes it all possible:

- Want to buy Tesla but only have $150? No problem—the system automatically calculates and purchases 0.46 shares

- Want to invest in Amazon? Enter $100 and the system automatically calculates the corresponding fractional share amount

- 100% capital utilization—every dollar can be immediately invested in the market to generate compound returns

Real-World Example: The first time I used fractional shares was to buy Shopify (SHOP), when the stock price was around $150-$170. I bought 1-2 shares with $200. Later in June 2022, they did a 1-for-10 stock split, increasing the number of shares, and that investment taught me about the rewards of long-term investing!

💰 Wealthsimple Cash: High-Interest Bank Account

In June 2025, Wealthsimple Cash was officially renamed Wealthsimple Chequing, offering higher interest rates than major banks.

2025 Interest Rates (as of November):

| Membership Tier | Base Rate | With Direct Deposit Bonus |

|---|---|---|

| Core (Regular users) | 1.25% | 1.75% |

| Premium ($100K+) | 1.75% | 2.25% |

| Generation ($500K+) | 2.75% | 2.75% |

🌍 The Ultimate Global Travel Card

The Wealthsimple Cash Card is a prepaid Mastercard with a little-known killer feature:

✅ Wealthsimple doesn’t charge foreign exchange transaction fees, though Mastercard applies approximately 1% currency conversion fee

✅ Global ATM fee refunds

Real Money-Saving Example: One user shared that while traveling in Mexico, using the Wealthsimple debit card for purchases saved them $150-200 USD in exchange rate fees compared to traditional credit cards, depending on spending amount, since there are no foreign transaction fees! In contrast, most credit cards charge 2.5%-3% in foreign transaction fees.

🪙 Wealthsimple Crypto: Canada’s First Regulated Cryptocurrency Platform

Wealthsimple Crypto is Canada’s first fully regulated cryptocurrency trading platform, currently offering over 140 cryptocurrencies.

Trading Fees (by membership tier):

| Tier | Base Rate |

|---|---|

| Core | 2.0% |

| Premium | 1.0% |

| Generation | 0.5% |

Staking Feature: Stake ETH, SOL, DOT, ADA, and other cryptocurrencies to earn passive income. Annual percentage yields vary by crypto asset, with official figures showing up to 9% (after deducting the platform’s 30% staking fee).

📊 Wealthsimple Tax: Free Tax Filing Solution

Every tax season, Wealthsimple Tax is one of Canada’s most popular free tax filing software options.

Core Features:

- ✅ Completely Free: Uses a “Pay What You Want” model

- ✅ Auto-Import: Connect to CRA My Account to automatically pull T4, T5, and other tax slips

- ✅ Smart Check: Automatically searches for hundreds of tax deduction items

- ✅ Maximum Refund Guarantee: If other software calculates a higher refund, Wealthsimple compensates the difference (up to $50)

- ✅ NETFILE Certified: Can be submitted directly to CRA without mailing

🎯 How to Open an Account? Complete Registration in 5 Minutes + Get $25 Bonus

📝 What You Need Before Opening an Account

You’ll need to prepare:

- ✅ Proof of Identity: Driver’s license or passport

- ✅ SIN Number: Social Insurance Number (required)

- ✅ Mobile Phone: To receive verification codes

- ✅ Bank Account: For deposits

🚀 Registration Process (Step-by-Step)

Step 1️⃣: Download the App or Visit the Website

- iOS Users: Search “Wealthsimple” in the App Store

- Android Users: Search “Wealthsimple” in Google Play

- Web Version: Go to wealthsimple.com

Step 2️⃣: Create Your Account

- Enter your email address

- Set a password (a strong password is recommended)

- Verify your email

Step 3️⃣: Enter Referral Code to Get $25 Reward 🎁

This is the most critical step!

Method 1: Use the Referral Link (Easiest) Go directly to wealthsimple.com/invite/HP6BUW, and the system will automatically apply the referral code.

Method 2: Manually Enter the Referral Code

- During the registration process, look for the “Have a referral code?” or “Referral code” field

- Enter: HP6BUW

- Confirm that “$25 bonus will be applied” is displayed

Method 3: Add Within 7 Days After Deposit If you’ve already opened an account but forgot to enter the referral code, as long as it’s within 7 days of your deposit:

- Log into the app

- Tap the “Gift Icon” in the top right corner

- Fill in HP6BUW on the Referral page and it will take effect

Step 4️⃣: Complete Identity Verification

- Enter personal information (name, address, SIN number)

- Upload ID documents (driver’s license or passport)

- Take a selfie for facial recognition

- Answer a few simple questions about your investment experience

In most cases, verification is completed instantly with no waiting required!

Step 5️⃣: Choose Your Account Type

Select based on your investment goals:

- TFSA (recommended for beginners): Tax-Free Savings Account

- RRSP: Registered Retirement Savings Plan

- FHSA: First Home Savings Account

- Non-Registered: Regular investment account

Step 6️⃣: Link Your Bank Account and Make a Deposit

Deposit Method Comparison:

| Method | Time | Maximum Limit |

|---|---|---|

| e-Transfer | 3 minutes | $3,000/24 hours (varies by bank) |

| Direct Deposit (auto-transfer) | 1-2 business days | No limit |

| Bank Transfer | 1-2 business days | No limit |

| Instant Deposit | Immediate | Varies by account type and credit limit ($50,000-$250,000) |

First Deposit Recommendation: Deposit $1-$100 (no need to invest a large amount right away). As long as your account is activated with at least $1 deposited, you’ll qualify for the $25 bonus.

✅ Done!

Within 24 hours, the $25 CAD bonus will be automatically added to your account. The reward must be kept for 180 days, or it may be reclaimed.

💡 Complete Guide to All Account Types

Choosing the right account type is more important than picking stocks! Here’s a detailed account comparison and strategy recommendations.

📊 Account Type Comparison Chart

| Account Type | Suitable For | Tax Benefits | Withdrawal Restrictions | 2025 Contribution Limit |

|---|---|---|---|---|

| TFSA | All Canadians | 0% tax | No restrictions | $7,000/year |

| RRSP | Retirement savings | Tax deduction on contributions | Withdrawals are taxed | 18% of previous year’s income, max $32,490 |

| FHSA | First-time homebuyers | Tax deduction + 0% growth tax | Can withdraw before home purchase | $8,000/year, lifetime $40,000 |

| RESP | Saving for child’s education | 20% government grant | Education purposes only | Lifetime $50,000 |

| Non-Registered | High net worth individuals | No tax advantages | No restrictions (must report taxes) | No limit |

💰 TFSA (Tax-Free Savings Account)

Core Advantages:

- All earnings within the account (capital gains, dividends, interest) are completely tax-free to the Canada Revenue Agency (CRA)

- Withdrawals are also completely tax-free

- Can withdraw anytime without penalties

Wealthsimple Strategy: This is the first choice for most people. Take advantage of Wealthsimple’s zero-commission feature to build a high-growth ETF portfolio (such as XEQT or VFV) within your TFSA.

Real Example:

- Annual contribution limit: $7,000 CAD (2025)

- After 1 year of investment, grows to $7,700 (7% return)

- After-tax net profit: $700 (traditional accounts would be taxed, here it’s 0%)

⚠️ Warning: Never engage in frequent day trading within your TFSA. The CRA may consider it a business activity and tax it accordingly.

🏡 RRSP (Registered Retirement Savings Plan)

Core Advantages:

- Contributed funds can deduct from your taxable income for that year (tax refund)

- Enjoy tax-deferred growth

- According to the Canada-US tax treaty, only RRSP and RRIF (retirement-related accounts) are exempt from the US 15% withholding tax. FHSA, TFSA, and RESP are not exempt and still subject to the 15% withholding tax.

Wealthsimple Strategy: If you hold US stocks with dividends (such as Coca-Cola, J&J), RRSP is the only account that can be exempt from the US 15% withholding tax. However, note that if Wealthsimple’s Core account hasn’t upgraded the USD feature, mandatory currency conversion costs may offset this tax advantage.

Suitable For:

- ✅ High-income earners (high marginal tax rate)

- ✅ Long-term retirement savings

- ✅ Don’t need short-term access to funds

🏠 FHSA (First Home Savings Account)

Core Advantages:

- Combines RRSP’s tax deduction feature with TFSA’s tax-free withdrawal feature (as long as it’s used for home purchase)

- Tax-free growth, but US stock dividends are still subject to 15% US withholding tax (like RRSP and TFSA)

- Can fully withdraw when buying a home, no penalties

Wealthsimple Strategy: This is currently Canada’s most powerful investment tool. Young investors are advised to prioritize maxing out their FHSA contribution limit ($8,000 per year). Since home buying is typically a medium-term goal, consider choosing lower-volatility assets.

Real Example: A stay-at-home mom shared: “I opened an RESP, and the government automatically matches my contributions.

For example, if you contribute $2,500 annually with income below $57,375, you can receive:

- Basic CESG: $2,500 × 20% = $500/year

- Additional CESG: $500 × 20% = $100/year

- Annual government grant: $600

- 3-year accumulation: $1,800 (not including Canada Learning Bond)

📚 Which Account Should Beginners Start With?

If you need access to funds in the short term or don’t have stable income: ✅ Prioritize choosing TFSA as your first account. All your investment earnings (dividends, capital gains) are completely tax-free, you can withdraw anytime without penalties, and it won’t affect your eligibility for government benefits.

If you have stable employment income and plan for long-term retirement savings: ✅ Open both RRSP and TFSA, and allocate according to tax goals:

- First put tax refunds and bonuses into RRSP (through tax deduction advantages)

- Then put regular savings into TFSA

- Maximize overall tax optimization

If you’re a first-time homebuyer: ✅ Prioritize opening FHSA (the newest account, launched in 2023)

📖 Complete Investment Process: From Account Opening to Your First Trade

🎯 Scenario 1: Buying Canadian Blue-Chip Stocks (Example: TD Bank, Ticker Symbol TD)

Step-by-Step Instructions:

- Search for the Stock

- Open the Wealthsimple Trade App → Tap the “Trade” button

- Search for the stock: Enter “TD” or “Toronto-Dominion Bank”

- Review Stock Information

- Current price (e.g., $95.50 CAD)

- 52-week high/low

- Dividend yield (TD approximately 4%)

- 1-year and 5-year performance charts

- Choose Purchase Method

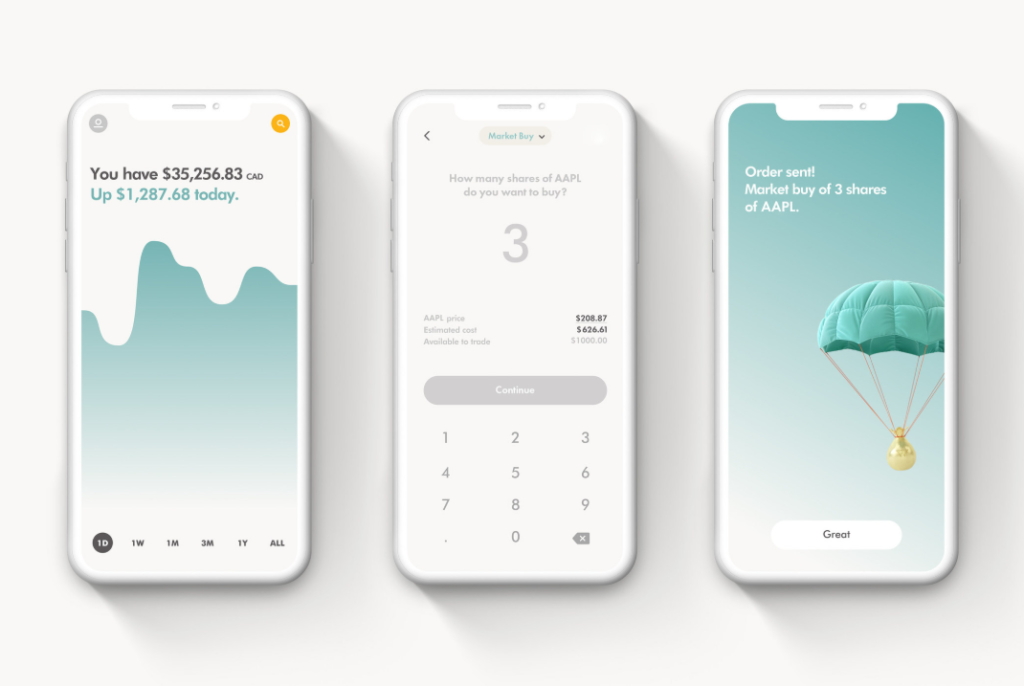

- Market Buy: Purchase immediately at the current market price

- Limit Buy: Set the maximum price you’re willing to pay (e.g., $94.00) and wait for execution

- Enter Number of Shares

- For example, 5 shares (Total cost: $95.50 × 5 = $477.50 CAD)

- Select Account

- Confirm which account to use for the purchase (TFSA, RRSP, etc.)

- Review and Confirm

- Ticker symbol ✓

- Number of shares ✓

- Estimated cost ✓

- No hidden fees ✓ ($0 Commission)

- Tap “Queue Order” to Confirm

Result:

- During market hours (Monday-Friday 9:30 AM – 4:00 PM EST): Instant execution

- Outside market hours: Order will execute automatically at the next market open

- Confirmation email will be sent

🇺🇸 Scenario 2: Buying U.S. Stocks (Example: Apple, Ticker Symbol AAPL)

Purchasing U.S. stocks involves currency conversion, so costs will be slightly higher:

- The process is the same, but the system will prompt “USD required”

- Wealthsimple will automatically convert: CAD → USD

- Conversion Fee:

- Core customers: 1.5%

- Premium customers: 1.5%

- Generation customers: 1.5%

Cost Calculation Example:

- Apple stock price: $240 USD

- Purchase 10 shares = $2,400 USD

- Foreign exchange fee (1.5%) = $36 CAD

- Total cost (CAD) = $2,400 × 1.35 + $36 = $3,276 CAD

📊 Scenario 3: Buying ETFs (Example: VGRO, Canadian Balanced ETF)

Why Choose ETFs Over Individual Stocks?

- ✅ Lower risk (One ETF contains 100+ companies)

- ✅ Automatic diversification (No need to manually select stocks)

- ✅ Extremely low fees (MER around 0.3%, far below mutual funds’ 2%+)

The process is identical to buying individual stocks—simply enter “VGRO” in the search bar.

💸 Complete Fee Structure Analysis: Hidden Costs Revealed

Understanding the fee structure is crucial when choosing an investment platform. Below is a detailed breakdown of all Wealthsimple fees.

✅ Canadian Stocks: Completely Free

When trading stocks and ETFs listed on the Toronto Stock Exchange (TSX) or TSX Venture (such as RY, TD, SHOP, VFV, XEQT), Wealthsimple is unbeatable.

- Commission: $0

- Platform fees: $0

- Data fees: $0

- Conclusion: For Canadian passive investors (Couch Potato Investors), this is the best option on the market

⚠️ U.S. Stocks: 1.5% Foreign Exchange Fee Explained

This is Wealthsimple’s biggest “hidden cost”. When you buy or sell U.S. stocks with a CAD account, you’re charged a 1.5% foreign exchange fee on each transaction.

How It Works:

- When buying U.S. stocks, the system automatically converts your CAD to USD, charging a 1.5% fee

- When selling U.S. stocks, the system automatically converts USD back to CAD, charging another 1.5% fee

Mathematical Impact: If you buy $1,000 USD worth of Tesla and immediately sell it, even if the stock price doesn’t change, assuming a WSII Corporate Exchange Rate of 1.30 CAD/USD, you’ve already lost approximately 3% (about $39).

Specifically: When buying, you pay $1,300 CAD to purchase $1,000 USD (1.5% fee charged), when selling, you receive $1,280.50 CAD (another 1.5% fee charged), for a net loss of approximately $19.50 CAD plus the initial purchase fee of $19.80, totaling about $39.30.

Foreign Exchange Fee Tier Table:

| Transaction Amount | FX Fee |

|---|---|

| Under $10,000 | 1.5% |

| $10,000-$24,999 | 1.0% |

| $25,000-$99,999 | 0.5% |

| $100,000+ | 0% |

💡 How to Save on Foreign Exchange Fees?

Method 1️⃣: Upgrade to Premium Membership

- Automatic upgrade with $100,000 in net deposits or total assets (whichever is higher)

- Gain access to a free USD account

- Foreign exchange fee remains at 1.5%

Method 2️⃣: Subscribe to USD Account

- $10/month (Core customers)

- Free for Premium/Generation customers

- Once activated, you can hold USD directly

- Pay conversion fee only once when funding the account

Break-Even Point Analysis: If you trade U.S. stocks frequently or make large transactions, the $10 monthly fee is far less than the 1.5% loss per trade.

Method 3️⃣: Use CAD-Denominated ETFs to Invest in U.S. Stocks

Purchase Canadian ETFs that track U.S. indices, such as:

- ZSP.TO (Tracks S&P 500)

- VFV.TO (Tracks S&P 500)

- XUU.TO (Tracks S&P U.S. Total Market Index)

These ETFs trade in CAD with no 1.5% foreign exchange fee.

📊 Premium and Generation Membership Explained

Premium (Assets $100,000+):

- ✅ Free USD account (saves $10/month)

- ✅ Management fee reduced to 0.4%

- ✅ Cash account interest rate of 2.25%

- ✅ Priority customer service

- ✅ Free Wealthsimple Tax Plus

- ✅ Partner perks (Uber, Headspace, etc.)

Generation (Assets $500,000+):

- ✅ Management fee as low as 0.2%

- ✅ Dedicated financial advisor team

- ✅ Up to 10 complimentary DragonPass airport lounge visits per year (requires redeeming 4 visits through milestone rewards + applying for Visa credit card for 6 additional visits)

- ✅ Cash account interest rate of 2.25%

- ✅ Private equity and private debt investment opportunities

- ✅ Medcan health services discount

- ✅ Generation members receive free upgrade to Wealthsimple Tax Pro

🔥 Advanced Features & Investment Tips

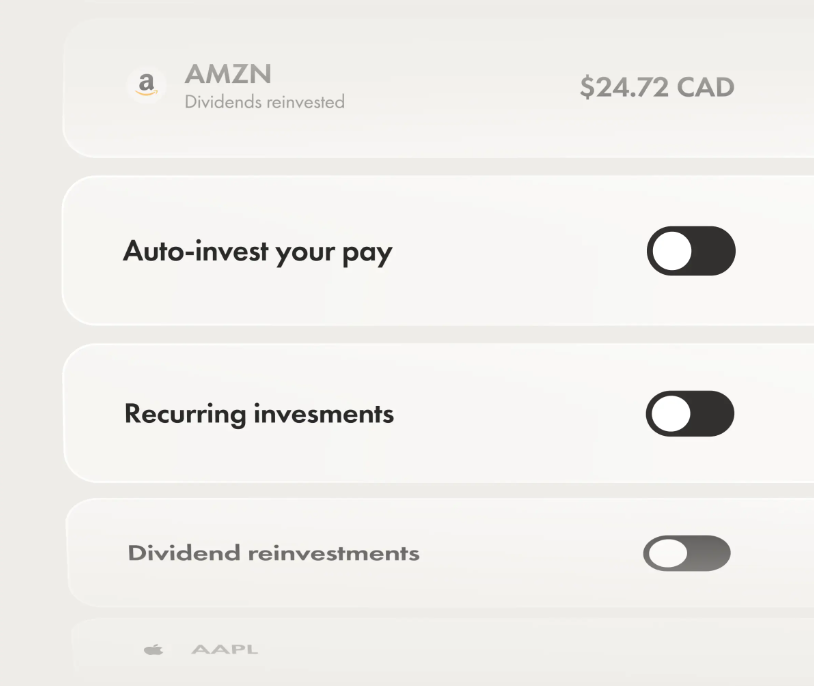

🤖 Tip 1: Set Up Automatic Investing (Dollar-Cost Averaging)

Instead of waiting for the “perfect timing” to invest (a common beginner mistake), set up recurring automatic investments.

How to Set It Up:

- Method 1: Search for the stock/ETF you want to buy → Click “Buy” → Select “Recurring Investment”

- Method 2: Click the “Move” tab at the bottom of the app → Select “Automations” → Set up recurring investment

- Configure:

- Stock/ETF (e.g., VGRO – Canadian Balanced ETF)

- Amount: $100/week

- Funding source: Bank account

The Result:

- $100 automatically transfers from your bank every week

- Wealthsimple automatically purchases your selected stock

- No manual intervention needed – your wealth grows automatically over 5 years

Real Success Story: Many users report that starting with $200/month automatic investments in 2020, their accounts have grown to $15,000+ after 5 years (including market returns)!

📉 Tip 2: Use Limit Orders to Lock in Target Prices

A common beginner mistake: using “Market Buy” directly, resulting in paying higher prices than expected.

The Right Way to Use Limit Orders:

- Search for a stock (e.g., Microsoft, MSFT)

- Click “Buy”

- Select “Limit Buy” instead of “Market Buy”

- Enter the price you’re willing to pay (e.g., if the stock is currently $400, set it at $395)

- Enter number of shares

- Check “Good Till Cancelled” (GTC)

- Place order

Benefits:

- ✅ Only executes when the stock drops to $395

- ✅ Can set long-term orders for up to 90 days (markets fluctuate, so it will likely trigger eventually)

- ✅ Prevents overpaying (protects against slippage during volatile markets)

💎 Tip 3: Enable Automatic Dividend Reinvestment (DRIP)

When purchasing dividend-paying stocks, you’ll receive regular cash dividends. Most beginners leave dividends in their cash account—but this wastes the power of compounding!

The Right Approach: Enable Automatic Dividend Reinvestment

In the Wealthsimple App:

- Click the gear icon (settings) in the upper right corner of the account page → Select “Automations” → Turn on “Dividend Reinvestment” (Note: This is an account-wide setting and cannot be configured for individual stocks)

- Enable it

The Result:

- Every time you receive dividends (typically quarterly), Wealthsimple automatically purchases more shares

- No manual action needed, automatic compound growth

- Account growth can reach 30-50% over 5 years (depending on market conditions and dividends)

🎁 Tip 4: Round-Up Investing

Link your spending account, and spare change from each card transaction will be automatically invested.

For example: Coffee costs $4.50, the system will automatically invest $0.50.

📊 Tip 5: Stock Lending (Share Lending Revenue)

Enable the stock lending feature to lend your held shares to other traders, and you’ll receive 50% of the revenue split.

⚖️ Wealthsimple vs Competitors In-Depth Comparison

📊 Complete Comparison Table (2025 Edition)

| Feature | Wealthsimple | Questrade | Moomoo | IBKR |

|---|---|---|---|---|

| Canadian Stock Commission | $0 | $0 | Min $1.49/trade | Low as $1 |

| US Stock Commission | $0 | $0 | $0.0099/share | $0.0035/share (tiered, min $0.35 USD/trade, max 1% of trade value) |

| Foreign Exchange Fee | 1.5% commission (WSII enterprise rate contains spread, actual spread floats) | 1.75% (or Norbert’s Gambit ~$12) | 1.1%-1.5% | 0.002% |

| USD Account | 30-day free trial, then $10/month (taxes included) | Free | Free | Free |

| Minimum to Open | $0 | $0 | $0 | $0 |

| User-Friendliness | ⭐⭐⭐⭐⭐ | ⭐⭐⭐ | ⭐⭐⭐⭐ | ⭐⭐ |

| Cryptocurrency Trading | 140+ types | None | None | Yes but high fees |

| Options Trading | $0/contract | $0.99/contract | $0.65/contract, min $1/trade | $1.5-$2 |

| Bonds/GICs | ❌ | ✅ | ❌ | ✅ |

| High-Interest Savings Account | Core 1.25%, Premium 1.75%, Generation 2.75% | None | None | None |

🎯 Which One Should I Choose?

Choose Wealthsimple if you:

- ✅ Are a beginner wanting a simple start

- ✅ Plan to hold Canadian stocks and ETFs long-term

- ✅ Want a complete financial ecosystem (investing + savings + cash card)

- ✅ Are interested in cryptocurrency

- ✅ Value user experience and app design quality

Choose Questrade if you:

- ✅ Focus on US stocks and want to save on FX fees

- ✅ Need bonds, mutual funds, and international stocks

- ✅ Are interested in options trading (lower fees)

- ✅ Are willing to learn a more complex platform

Choose Interactive Brokers if you:

- ✅ Are an advanced trader needing global market access

- ✅ Engage in high-frequency trading or complex strategies

- ✅ Have $100,000+ in assets (platform complexity is worth it)

⚠️ 5 Key Drawbacks of Wealthsimple & Solutions

No platform is perfect. For a fair evaluation, we must also highlight Wealthsimple’s limitations.

❌ Drawback 1: 1.5% FX Fee on US Stock Trades (Core Customers)

The Issue: Compared to Questrade (which supports Norbert’s Gambit for zero-cost currency conversion), Wealthsimple charges a 1.5% FX fee on each US stock transaction.

Solutions:

- ✅ Upgrade to Premium ($100K+ auto-upgrade) → FX fees are tiered based on trade amount ($10,000-$24,999 at 1%; $25,000-$99,999 at 0.5%)

- ✅ Make larger, one-time US stock purchases (reduce transaction frequency)

- ✅ Use Questrade as a “secondary account” specifically for US stocks

❌ Drawback 2: No Norbert’s Gambit Support (Currency Arbitrage)

What is Norbert’s Gambit? A legal tax strategy that allows zero-cost conversion between CAD and USD through cross-trading stocks and ADRs (American Depositary Receipts).

The Impact: If you need large USD investments (e.g., $50,000+), Norbert’s Gambit could save you $750+.

Solutions:

- ✅ For small US stock investments (<$10,000): Wealthsimple’s 1.5% fee is acceptable

- ✅ For large US stock investments (>$20,000): Open a Questrade account and use Norbert’s Gambit

- ✅ Wait until Q1 2026: Wealthsimple is expected to support Norbert’s Gambit

❌ Drawback 3: No Bonds or GICs (Fixed Income Products)

The Issue: Wealthsimple only offers stocks, ETFs, and cryptocurrency.

Alternatives:

- ✅ Purchase “Bond ETFs” (e.g., XGB – Canadian Bond ETF) for similar returns

- ✅ Open GICs at traditional banks (typically 4-5% rates)

- ✅ Keep cash in your account balance (Wealthsimple Core account 1.25% or Premium account 1.75%; if assets reach $500,000 upgrade to Generation for 2.25%)

❌ Drawback 4: 15-Minute Market Data Delay

The Issue: Stock prices displayed in the Wealthsimple App are “delayed quotes” from 15 minutes ago.

Solutions:

- ✅ Beginners shouldn’t day trade anyway (extremely high risk)

- ✅ When using Limit Orders, the system still uses real-time market prices at execution

- ✅ If you need real-time quotes, check Yahoo Finance or Google Finance simultaneously

❌ Drawback 5: Limited Research Tools

The Issue: Wealthsimple’s analytical tools are very basic compared to Questrade or Interactive Brokers.

Solutions:

- ✅ Use free external tools: Yahoo Finance, Seeking Alpha, TradingView

- ✅ Wealthsimple is positioned as a “long-term investment platform,” not a “trader’s workstation”

- ✅ Beginners should learn investment fundamentals first, then consider advanced analysis

🚫 5 Major Investment Traps Beginners Should Avoid

⚠️ Trap 1: Choosing the Wrong Account Type Leading to Excessive Taxation

Common Mistake: Opening a “Non-Registered” account, resulting in heavy taxes on investment gains.

Solution:

- ✅ Maximize your TFSA first (annual limit: $7,000)

- ✅ Then utilize your RRSP (higher annual limit)

- ✅ Only use Non-Registered accounts last

Tax Impact Example ($10,000 investment, $1,000 gain after 1 year):

- TFSA: $0 tax

- RRSP: Tax-deferred (taxed only upon withdrawal)

- Non-Registered: $150-300 tax (depending on marginal tax rate)

⚠️ Trap 2: Buying High and Panic Selling

Psychological Barrier: FOMO (fear of missing out) drives you to buy when stocks rise, then panic selling during short-term declines.

Data: Statistics show that frequent traders achieve an annual return of 11.4%, while buy-and-hold investors achieve 18.5%, meaning frequent traders earn approximately 38% less.

Solution:

- ✅ Set up automatic investment plans ($100-500 monthly) to avoid emotional decisions

- ✅ Use limit orders to set “the maximum price you’re willing to pay”

- ✅ Avoid daily charts; focus on 1-year+ trend charts instead

⚠️ Trap 3: Hidden Costs from Over-Trading

The Problem: Even with Wealthsimple’s zero commission, frequent trading still increases:

- ❌ Tax complexity (need to track cost basis for every transaction)

- ❌ Psychological burden (constantly checking accounts leads to impulsive decisions)

- ❌ Currency exchange risk (every US stock trade exposes you to exchange rate fluctuations)

Statistics: Research shows that frequent traders (more than 48 trades annually) underperform market indices by 86 basis points monthly, equating to 10.3% annually. Meanwhile, buy-and-hold strategies typically maintain market average returns (approximately 8-10% annual returns).

Solution:

- ✅ Establish a “buy and don’t look” discipline

- ✅ Set 3-5 year holding targets

- ✅ Only sell when fundamentals change

⚠️ Trap 4: Ignoring Tax-Loss Harvesting Opportunities

Concept: If a stock is at a loss (e.g., bought at $100, current value $80), actively selling to “realize the loss” allows you to use that $20 loss to offset $20 in gains from other investments, legally reducing your taxes.

Wealthsimple Advantage: Premium and Generation clients can enjoy automatic tax-loss harvesting features in “Managed Investing accounts.” This feature is not available for Self-Directed accounts.

Manual Execution Method:

- Review your account every December

- Identify losing positions

- Sell to “realize the loss”

- Record the loss amount

- Offset capital gains from other stocks

⚠️ Trap 5: Investing in Only One Stock or Sector

Beginner Mistake: “Tesla is so great, I’ll put all my money into it.” Result: Tesla drops 30%, and your entire portfolio crashes.

Solution (Diversified Portfolio Template):

- ✅ 50% Canadian broad market ETF (VGRO or XGRO)

- ✅ 20% US equity ETF (VFV or XUU)

- ✅ 20% Individual stocks (companies you’re confident in, like TD, Enbridge)

- ✅ 10% Cash (emergency reserve)

Results:

- 60% reduction in risk

- Returns can still reach 7-10% annually

- A downturn in any market sector won’t devastate your entire portfolio

🙋 Frequently Asked Questions (FAQ)

When will I receive the $25 bonus from using referral code HP6BUW?

A: The bonus is typically credited automatically within 24 hours after completing your account setup and depositing at least $1. It will appear in your cash account balance. If you don’t see it, contact Wealthsimple customer support to verify the referral code was entered correctly.

Does referral code HP6BUW have an expiration date?

A: The referral code itself is valid long-term, but if you want to add a referral code after opening your account, you must do so within 7 days of your first deposit. This 7-day time limit is strictly enforced. Make sure to complete this step as soon as possible after opening your account.

Can I open multiple accounts at the same time? For example, both a TFSA and RRSP?

A: Yes, you can. In fact, it’s highly recommended to open both TFSA and RRSP accounts, as they offer different tax advantages and contribution limits. You can easily add multiple accounts within the Wealthsimple app, and funds and investments can be freely transferred between accounts.

Should I choose TFSA or RRSP?

A:

- Choose TFSA: Lower income, need fund flexibility, short to medium-term investment goals

- Choose RRSP: High income earners (high marginal tax rate), long-term retirement savings

- Use both: If you have sufficient funds, open both accounts

What is FHSA? Is it worth opening?

A: FHSA (First Home Savings Account) combines the benefits of both RRSP and TFSA: contributions are tax-deductible, growth is tax-free, and withdrawals for home purchases are also tax-free. If you’re planning to buy your first home in Canada, this is currently the most advantageous account type.

What happens to my money if Wealthsimple goes bankrupt?

A: Your funds are protected by dual coverage:

- CIPF protection: Investment accounts protected up to $1 million CAD

- CDIC protection: Cash accounts protected up to $1 million CAD

This means even if Wealthsimple goes bankrupt, your funds remain completely safe. Furthermore, Wealthsimple completed a CAD $750 million funding round in October 2025, co-led by global top-tier investment firm Dragoneer Investment Group and Singapore sovereign wealth fund GIC, reaching a company valuation of CAD $10 billion, making bankruptcy extremely unlikely.

Can non-Canadian citizens use it?

A: As long as you are a Canadian tax resident, have a SIN number, and meet the legal age requirement in your province, you can open an account. New immigrants with work permits or PR status can also use it.

Is Wealthsimple really free? Are there any hidden fees?

A: Trading Canadian stocks and ETFs is indeed free. The main “hidden” fee is the 1.5% foreign exchange conversion fee when buying and selling US stocks. Additionally:

- Cryptocurrency trading fees: Core members 2.0%, Premium members 1.0%, Generation members 0.5% (lower rates available based on total trading volume within 30 days)

- Wealthsimple Invest management fee: 0.4%-0.5%/year

- USD account subscription: $10/month (free for Premium and above)

How can I avoid the 1.5% foreign exchange fee?

A: There are three methods:

- Subscribe to USD Account for $10/month

- Reach $100,000 in assets to upgrade to Premium and get USD account for free

- When account assets exceed $100,000, US stock trading foreign exchange fee drops to 0%

Is Premium membership worth it?

A: If you: (1) frequently trade US stocks, (2) have assets approaching $100,000, (3) use Wealthsimple managed investments—then Premium is definitely worth it. The free USD account alone saves you $120+ per year, and the foreign exchange fee savings are even more substantial.

What’s the minimum investment amount?

A: $0. You can open an account and complete verification first, then deposit funds later. Using referral code HP6BUW only requires depositing $1 to receive the $25 reward.

Can I buy US stocks?

A: Yes. Wealthsimple supports stocks and ETFs listed on US exchanges like NYSE and NASDAQ. However, be aware of the 1.5% foreign exchange fee.

How long does it take to withdraw funds?

A: Standard withdrawals take 1-3 business days. Instant withdrawals (requires linking a Visa Debit card that supports Instant Funds Movement) are submitted to the bank immediately, though actual deposit time still depends on your card issuer’s processing speed, and incur a 2.5% fee. Recently deposited funds require a 5-business-day waiting period before withdrawal.

Are real-time quotes available?

A: Yes. Wealthsimple provides free real-time streaming quotes with no additional charges.

Can I use Wealthsimple for day trading?

A: Technically yes, but not recommended. The lack of Level 2 data, rudimentary charting tools, and USD trading costs make it unsuitable as a frequent trading tool. It’s better suited for swing trading or long-term investing.

Why do people say Wealthsimple’s cryptocurrency fees are high?

A: Yes, they are. Wealthsimple Crypto charges based on user tier: Core tier 2%, Premium tier 1%, Generation tier 0.5% (charged on both buy and sell). Combined with the spread Wealthsimple typically charges (an additional 0.5-2%), actual total fees can reach 3-4%. Compared to professional exchanges (like Binance, Kraken) charging 0.1%-0.5%, this is indeed expensive. However, for ordinary users who just want to allocate a small amount to Bitcoin without managing private keys, the premium is for compliance and convenience.

What is “Norbert’s Gambit”? Does Wealthsimple support it?

A: This is a technique that uses stocks listed in both US and Canadian markets to perform near-zero-cost currency exchange. This feature is expected to launch in early 2026.

Will Wealthsimple have a credit card?

A: Yes, the Wealthsimple Visa Infinite credit card is being rolled out to select users, offering 2% flat-rate cash back.

🎯 Real User Testimonials

💬 Case 1: 28-Year-Old Software Engineer

“I started with $50 in 2020 to try it out, and now (in 2025) my account has grown to $18,000. With a traditional bank, fees alone would have cost me over $1,000. Wealthsimple changed my perspective on investing—it showed me that even with just $50, I could start building wealth.”

💬 Case 2: 35-Year-Old Married Individual

“I opened a Wealthsimple Cash card before my Mexico vacation. During the 3-week trip, compared to traditional credit cards, I saved $350 in exchange rate fees. When I got back, I immediately transferred all my bank accounts to Wealthsimple—it’s such a great deal.”

💬 Case 3: New Mom

“As a stay-at-home mom, I don’t have a steady income. But I opened an RESP, and the government contributions automatically go into investments. After 3 years, I’ve saved $15,000 for my son, with $3,000 being free money from the government. Wealthsimple made it easy to achieve my goal of financial planning for the next generation.”

💬 Case 4: My Personal Experience

My first purchase was Shopify (SHOP) when the stock price was around $100+. I bought 2 shares with $200. After the stock split and price surge, that investment truly showed me the power of compound returns. Of course, I’ve also made mistakes, buying some “hot recommended” stocks that I eventually sold at a loss. These experiences taught me: don’t put all your eggs in one basket—regular ETF investing is the key to long-term profitability.

✨ Conclusion and Action Steps

🏆 Why Choose Wealthsimple?

After a comprehensive in-depth review, the conclusion is clear: for 90% of average Canadian investors, Wealthsimple remains the best choice.

Core Advantages Summary:

- ✅ Zero commission (Canadian stocks & ETFs)

- ✅ Start with $1 (world’s lowest minimum)

- ✅ 5-minute account opening (instant activation)

- ✅ $25 sign-up bonus (use referral code HP6BUW)

- ✅ High-yield savings (up to 2.25% interest rate, 1.25% for regular customers)

- ✅ No hidden fees (completely transparent pricing)

- ✅ Comprehensive ecosystem (investing + savings + crypto + tax filing)

It may not be the most professional (that’s IBKR’s territory), nor have the cheapest currency exchange (that’s currently Questrade’s advantage), but it’s the most balanced, user-friendly platform with the strongest ecosystem.

🚀 Start Now: 3-Step Action Plan

Step 1: Sign Up Immediately (5 minutes)

🎁 Use referral code HP6BUW to open an account and receive a $25 bonus 📱 Click the link or enter the referral code: wealthsimple.com/invite/HP6BUW

Step 2: Deposit $1-$100 (3 minutes)

💳 Via e-Transfer, direct deposit, or bank transfer

Step 3: Buy Your First ETF (2 minutes)

📊 Search for “VGRO” or “XEQT“, click “Buy”

✅ Done!

Within 24 hours, you will receive:

- 💰 $25 referral code bonus

- 📈 Your first share ownership

- 🎯 Your first step toward financial freedom

📚 Appendix: Quick Reference Data Table

| Item | Data/Terms | Notes |

|---|---|---|

| Referral Code | HP6BUW | $25 bonus, requires deposit to activate |

| Canadian Stock Commission | $0 | Buy and sell commission-free |

| US Stock FX Fee | 1.5% | Waived with USD account ($10/month) |

| Cash Interest Rate | 1.25%-2.25% | Based on asset tier and Direct Deposit |

| Crypto Fee | 0.5%-2% | Decreases with tier level |

| Deposit Insurance | CDIC(Cash)/CIPF(Trade) | Up to $1M CAD coverage |

| Account Opening Time | Few minutes | Instant activation |

| Minimum Investment | $1 | Supports fractional shares |

| User Base | 3+ million | 2025 data |

| Assets Under Management | $100 billion CAD | Surpassed in October 2025 |

Disclaimer: This article is for educational and informational purposes only and does not constitute specific investment advice. Financial markets involve risks. Please conduct independent research or consult a licensed financial advisor before investing. All fee and feature information is sourced from Wealthsimple’s official website and is subject to change. Please refer to official announcements for the most current information.

💭 Final Thoughts

Investing isn’t an exclusive game for the wealthy. Thanks to Wealthsimple, anyone—regardless of capital, age, or background—can start investing in their future with minimal cost and maximum simplicity.

You don’t need to wait for the perfect moment, you don’t need substantial capital, and you don’t need complex knowledge.

All you need is:

- 📱 An account application form

- 💵 $1 CAD

- ⏰ 3 minutes of your time

The rest? Leave it to the magic of compound interest.

🎁 Referral Code Quick Link

🎁 Don’t forget to use referral code HP6BUW to claim your $25 sign-up bonus! It’s the easiest first “profit” on your investment journey.

Open Account Now: wealthsimple.com/invite/HP6BUW

Terms: Open an account and deposit any amount (minimum $1) within 30 days to receive a $25 CAD bonus. Additional offers include matching bonuses (deposit $25,000+ for 1-2% bonus, up to $40,000).

📈 Conclusion: Start Your Investment Journey Today

Wealthsimple has truly transformed the way Canadians invest. For beginners, it offers the lowest entry barrier and most user-friendly experience on the market. For investors seeking simplicity, the all-in-one platform eliminates the hassle of switching between multiple apps.

Of course, no platform is perfect. If you’re an active trader, you may need to consider other options. But for most people—especially those just starting their investment journey—Wealthsimple remains the most recommended investment platform for Canadians.